Fraud Management & Cybercrime

,

Fraud Risk Management

,

ID Fraud

Credit Washing, Synthetic ID Fraud and Bust-Out Fraud Are Among the Usual Suspects

Auto lenders are grappling with a surge in complex fraud schemes that are not only increasing in volume but also exploiting systemic blind spots. From coordinated bust-out rings to fake dealership websites, fraudsters are expanding their playbooks with bold new tactics.

See Also: Optimizing AppSec in the Financial Services Sector

Even fringe fraud tactics such as credit washing and synthetic identity creation have become mainstream, posing growing risks to both lenders and consumers in an already strained economic climate.

According to Point Predictive’s 2025 Auto Lending Fraud Trends Report, fraud losses climbed to $9.2 billion, up 16.5% over 2023 losses. First-party fraud, including income misrepresentation and credit washing, now accounts for 69% of all types of fraud, highlighting how “legitimate-looking” borrowers are abusing the system.

Identity-related schemes such as synthetic identity fraud, true name identity theft and credit washing now represent 45% of all auto lending fraud, a 41% jump over the previous year. Frank McKenna, chief strategist at Point Predictive, attributed the rise in fraud in the auto lending market to a “combination of economic pressure, digital convenience and inadequate verification controls.”

For example, inflation and rising interest rates have squeezed borrowers, while layoffs at tech giants have left many workers without safety nets. As a result, borrowers are more likely to commit first-party fraud by giving false income information or using credit repair scams to hide debt from their records.

The report found that credit washing alerts rose by 162% in 2024. Synthetic identity fraud climbed to 525.3 points on Point Predictive’s Synthetic Identity Risk Index – five times more than its 2017 baseline.

Bust-Out Fraud: Luxury Cars and Fake LLCs

Bust-out fraud rose another 6.5%, growing on a 27% increase the year before. Using this tactic, fraudsters build up legitimate credit histories by using either their real identities or synthetic identities and max out credit lines before busting out and vanishing.

In one case, a Florida-based crime ring – dubbed the “South Beach Bust Out Syndicate” – submitted more than $10 million in fraudulent applications for high-end vehicles such as BMW and Mercedes. The syndicate inflated incomes to an average of $284,000, often using fake transportation-related LLCs as employers.

After acquiring vehicles, the fraudsters deployed multiple tactics to monetize them: shipping cars overseas in containers, altering VINs to create untraceable ghost cars or subleasing them illegally on platforms such as Turo.

“Bust-out scams have emerged in this sector for the first time this year. Unfortunately, the main sufferers are the banks, who lose a large amount of money. The only solution is proper identity verification and information sharing,” McKenna said.

Credit Washing Goes Mainstream

Credit washing is now a mainstream tactic used by both consumers and organized networks. It involves filing false identity theft claims to remove negative entries from credit reports.

Credit washing alert rates have skyrocketed from 0.5% in 2022 to 1.7% in 2024, translating to nearly 1 in every 59 auto loan applications showing signs of manipulation. Unscrupulous credit repair companies are adding to the problem by convincing people in debt to erase poor credit histories and create a new identity using “credit profile numbers,” which are essentially unissued Social Security numbers or, in some cases, someone else’s Social Security number.

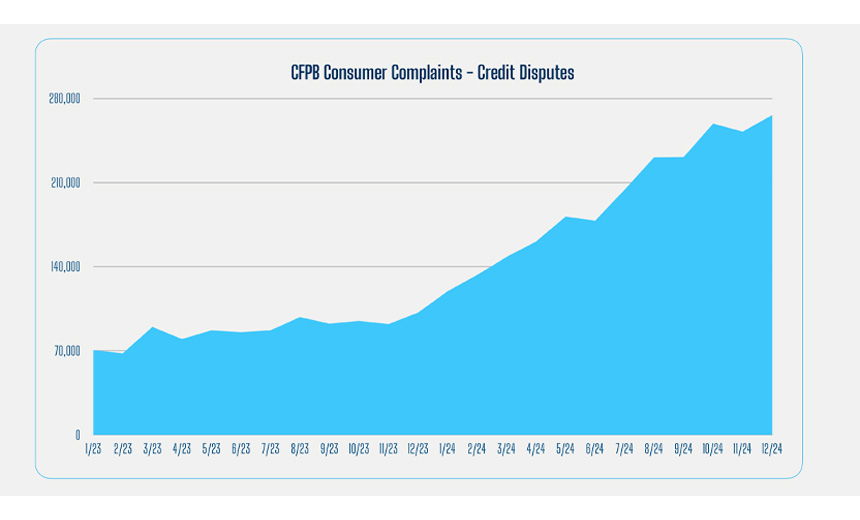

Federal regulators are also seeing sharp increases in fraud. The Consumer Financial Protection Bureau received 270,000 credit-related complaints in December 2024 alone, up from 70,000 in early 2023 – a 285% increase.

Fake Car Dealerships

Another new trend is the emergence of fake dealerships. Fraudsters have been building websites posing as legitimate car dealers and complete them with falsified inventory, phone numbers and financing options to lure victims and bypass lender controls.

Others fraudsters are manipulating employment data using shell companies set up to pass employment verification. In 2024 alone, this scam accounted for $3.9 billion in fraud risk.

1 Out of Every 114 Applications Is Synthetic

Synthetic identity fraud has become the most dangerous trend in auto lending. According to Point Predictive, the synthetic identity attack rate hit 88 basis points in 2024, meaning 1 out of every 114 applications involves a fake identity.

Fraudsters use CPNs to create new personas, sometimes recycling the same identity across multiple states. Houston remained the top city for synthetic identity fraud, followed by Chicago and Miami. Austin, Texas, showed the fastest year-over-year growth at 45%, while Tampa, Florida, had the highest overall synthetic fraud rate at 2.09% of applications.

“With emerging threats like AI-generated fake documents, deepfake-powered impersonation and fraud-as-a-service models flourishing on Telegram, the line between cybercrime and credit fraud is blurring,” McKenna said. “Without systemic change, the $9.2 billion in losses seen in 2024 may only be the beginning.”