AI-Based Attacks

,

Fraud Management & Cybercrime

,

Fraud Risk Management

Similar Fraud Rates Across Documents Reveal Weaknesses in Verification Workflows

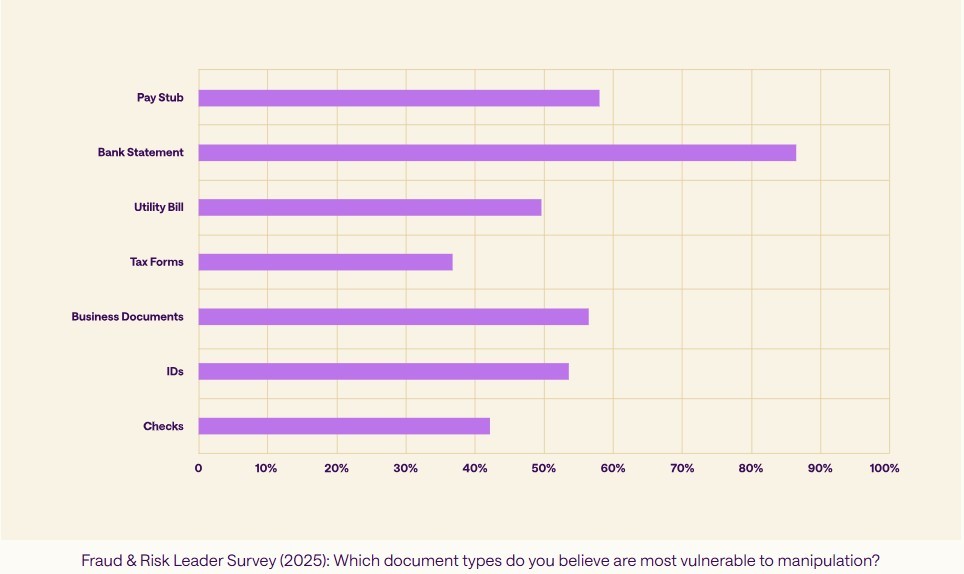

One in 16 documents processed across financial institutions last year showed signs of manipulation, fabrication or misrepresentation. For most fraud teams, this statistic triggers a familiar response that includes a call for better document detection and tighter review queues. But financial institutions may be looking in the wrong place. The real problem is not the documents. It’s the verification architecture built around them.

See Also: Experts Offer Insights from Theoretical to the Realities of AI-enabled Cybercrime

The latest report from InScribe’s 2026 State of Document Fraud, shows rates of fraud are nearly identical across every major document type. Bank statements, pay stubs, tax forms are all hovering between 4% and 7%. Experts say that this signals that fraudsters are not targeting specific documents. They’re probing verification workflows for the weakest entry point, then exploiting it.

Fraud has also evolved structurally. That vulnerability is compounded by how fraud has evolved structurally. InScribe found that the share of documents showing both identity and financial manipulation jumped from 40.2% in 2024 to 59.8% in 2025.

Fraudsters are no longer submitting a single doctored document. They’re building internally consistent fraud packages, a fake pay stub combined with a fake bank statement, supported by a fabricated employment letter designed to defeat verification systems that evaluate each document in isolation. Laura Spiekerman, co-founder of Alloy, commented that the categories are blurring and while some details are fake, some are correct as well.

Utility bills tell a similar story. The report says utility bills carry a higher fraud rate than most other document categories. This is not because these documents are easy to fake. Fraud reviewers treat this as a supporting document and not a primary one. As a result, it attracts less scrutiny. And this is the gap fraudsters exploit.

Fraudsters look for moments where a reviewer’s guard drops. Experts call this the architecture problem in its simplest form: Institutions assign scrutiny based on how they perceive document importance, not based on where fraud pressure actually lands. When those two factors diverge, fraudsters fill the gap. Verification systems designed to inspect individual documents were never built to detect broader fabrication ecosystem.

Fixing this requires rethinking where document verification sits within the broader risk workflow and not just focusing on improving the verification itself. This contextual framing also has direct implications for how institutions think about friction.

Frank McKenna, chief fraud strategist at Point Predictive, said that the industry’s current approach gets the targeting wrong.

“Too many companies do not realize that the overwhelming majority of applicants are honest. Fraud is still a relatively rare event, and so friction needs to be applied to just a small number of accounts or applications. Many lenders might request paystubs to verify customers on every single application when statistically less than 10% of applicants will actually be misrepresenting their income. The 90% suffer so the lender can find those few bad apples.”

McKenna believes the next evolution will render document-by-document verification almost entirely inadequate. “The next evolution will be artificial intelligence-created synthetic identities where scammers can create thousands of synthetic identities a day by choosing the best stolen Social Security number and pairing it with the right age, name and address so that it won’t raise a flag,” he said.

AI will be used to populate public records, manipulate credit records and then create perfect supporting documentation to back it up. The scale of this will be enormous and require banks to deal with a significant influx in fraud far beyond what they are receiving today.

For institutions still running siloed, document-by-document verification, it’s not a distant warning. The architecture that will fail them is already in place. The question is whether banks and other lenders redesign it before fraudsters finish mapping every gap in it.